A quick reaction to an interesting – but somewhat flawed – Bloomberg article that compared US and Chinese nominal GDP growth in 2023.

“US gross domestic product rose 6.3% in nominal terms — unadjusted for inflation — last year, outpacing China’s 4.6% gain.“

“While some of the outperformance reflected America’s elevated price increases, the 2023 outturn underscores a broader point: The US economy is emerging from the pandemic period in a better place than China’s.“

For starters, there is the issue of comparing one economy that notably experienced inflation (the US) with another that experienced notable deflation (China), while measuring them in the former’s currency. But, it does make for a captivating chart:

Caveats

Market indicators outside of GDP do collectively reveal a significant slowdown in China’s economy – yet, data from late 2023 indicates a gradual, U-shaped recovery, albeit heavily patchy.

This is a key issue in comparing the Chinese and US economies right now: they are in different stages of their respective post-pandemic recoveries.

While the US began its recovery from COVID-19, China’s economy suffered a more severe setback due to stringent shutdowns, more so than anything experienced in the West. As a result, the current state of the Chinese economy more closely resembles that of the US economy during 2021-22.

Peak China?

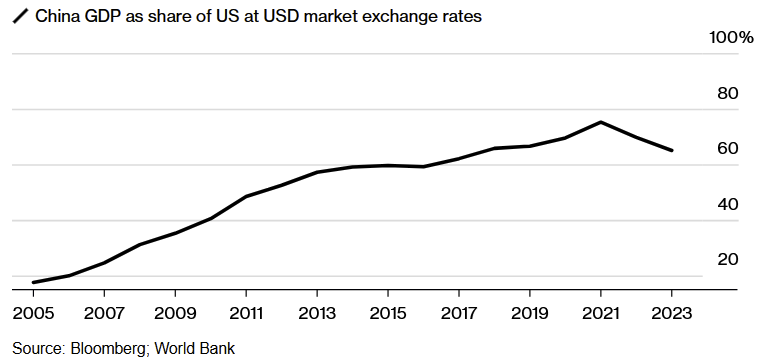

Oddities and caveats aside, this proclamation has introduced a concept to the mainstream. There is a school of thought among China watchers that 2018-2021 was perhaps ‘Peak China’ without us realizing it at the time. As it suggests, this was when China was relatively ahead of the world in not just economic growth, but also consumer confidence, social stability, and advancements in technological applications. This is when China was economically closest to reaching the US (nearly touching 80% the size of the US economy in 2021) before the gulf expanded again. This would also be before climate and demographic issues are expected to hit China the hardest.

Under this framing, Peak China could have lasted much longer if it were not for the trade war, the pandemic, and US export controls. From a geoeconomic perspective, the US has been quite successful – under both Trump and Biden – at stifling Chinese growth.

However – an argument against this is that China, although slowed for now, is far from out. The momentum and drivers of Chinese clout around the world are still very much present, and its hard power capabilities have far from peaked. Technological advancements may be slowed by difficulties in procuring advanced chips, but with the amount of scientific momentum and state-directed funding that will still be heavily prioritized, Chinese progression on these front cannot be expected to stay static.

Even if we take a plateauing economy to be the case, this is far from indicating a downturn in ambitions and investments towards areas that have likely yet to peak. Or more succinctly, a slowed China is far from a weakened China.

American Resurgence?

There are clear implications of this for domestic US politics, which can in turn affect the elections and thus US foreign policy. Either to the public or behind closed doors, both parties could sell the fact that their policies installed the speed bumps on China’s rise.

The Biden administration has done a great deal to instill frustration in Chinese policymakers with export controls, the Inflation Reduction Act, the CHIPS Act, and more. Yet, the Trump campaign could point to his administration being the one to kick off the trade war, transform US trade policy towards protectionism, and threaten the use of further measures to which the Biden administration simply carried into term.

Some of these may be truths or only half-truths, but the key is that both sides have ammunition in storage, strengthened by the potential narrative presented by these datapoints.

Extracting ourselves from from domestic considerations, it is nevertheless difficult to see US geopolitical power dramatically improving, even if it were buoyed by a strong economy. Can the US leverage this to assuage European difficulties and more thoroughly counter Russia? Can this lead to more impactful negotiations in the Middle East? Will Asia – including southeast Asia and India – coalesce around and align with US interests in the region?

The answers are murky. The tricky yet defining aspect of this century is the lack of a clear dividing framework between the interests of one power and the next.

To oversimplify it, America may have beaten the declining power allegations. But it still needs to play an astute multipolar game.